- Article Summary

-

Introduction

New international standards released in March 2026 mean that companies in food, agriculture, forestry, and dozens of related sectors now face binding requirements to measure and reduce the greenhouse gas emissions tied to their land use and supply chains. The Science Based Targets initiative (SBTi), the global body that validates corporate climate commitments, updated its land and agriculture emissions framework this year with tighter rules on who must act, new mandatory public commitments, and stricter accounting requirements. This article explains what those requirements are, who they apply to, and what decisions executives need to make now.

Key Takeaways

- Land and agriculture activities account for approximately 22% of global greenhouse gas emissions (IPCC, 2022). New rules require companies in affected sectors to set targets for this portion of their emissions separately from their energy and operations targets. Companies in six designated sectors including food production and forest products are required to act.

- Companies in other sectors may also be required if land-related emissions exceed 20% of their total footprint.

- A mandatory public commitment to eliminate deforestation from supply chains is now required as part of the target-setting process, with a hard deadline of December 31, 2030.

- Land-based emission reductions and carbon sequestration must be tracked and reported separately from energy and industrial emission reductions and cannot be used to offset fossil fuel obligations.

Why Land Emissions Are Now a Board-Level Issue

For most companies, climate strategy has focused on energy use, manufacturing, and transportation. But a significant share of global emissions originates from a different source: the land. Farming, deforestation, soil degradation, and changes in how land is used together contribute approximately 22% of all human-caused greenhouse gas emissions globally, around 13 billion tonnes of CO2 equivalent per year (IPCC, 2022).

The SBTi developed a dedicated framework for this category of emissions, known as the FLAG framework (Forest, Land and Agriculture). The land sector could contribute up to 37% of the emissions reductions and removals needed to stay within 1.5 degrees Celsius of warming through 2030, and 20% through 2050 (Griscom et al., 2017), making it one of the highest-leverage areas for corporate climate action. At the same time, the World Resources Institute (2019) projects that agricultural production is expected to increase by approximately 50% by 2050 to meet rising food demand, meaning decarbonization must occur alongside production growth.

For executives in food, agriculture, consumer goods, retail, and forest products, the 2026 update to this framework is a compliance requirement with defined deadlines, not a voluntary ESG initiative.

Who Must Set Land Emissions Targets

The updated rules specify two situations where a company is required to set a dedicated land emissions target, separate from its existing energy and operations targets.

The first situation covers companies in specific industries where land-related emissions are inherent to the business model. These are: Forest and Paper Products (Forestry, Timber, Pulp and Paper, Rubber); Food Production covering both agricultural and animal source businesses; Food and Beverage Processing; Food and Staples Retailing; and Tobacco.

The second situation applies to any company in any other sector where land-related emissions exceed 20% of total gross emissions across all scopes. Gross emissions means the raw total before any carbon credits or sequestration are netted out. Companies in retail, packaging, textiles, hospitality, construction materials, and consumer goods should assess whether their supply chain emissions include significant land components that could push them past this threshold.

Two groups are exempt. Small and medium-sized enterprises as defined by the SBTi are not required to comply. Companies operating in a designated sector but with very limited land-related emissions, below 5% of total emissions, are also excluded, though those emissions must still be accounted for within their overall reporting.

If your company already has validated science-based climate targets but has not yet set land emissions targets, the updated rules require you to do so no later than your next mandatory five-year target review, with the guidance stating this should happen as soon as possible.

What “Land Emissions” Actually Means in Practice

A common challenge executives face is understanding precisely what falls within scope. Land emissions are broader than most companies initially expect, and they extend deep into supply chains.

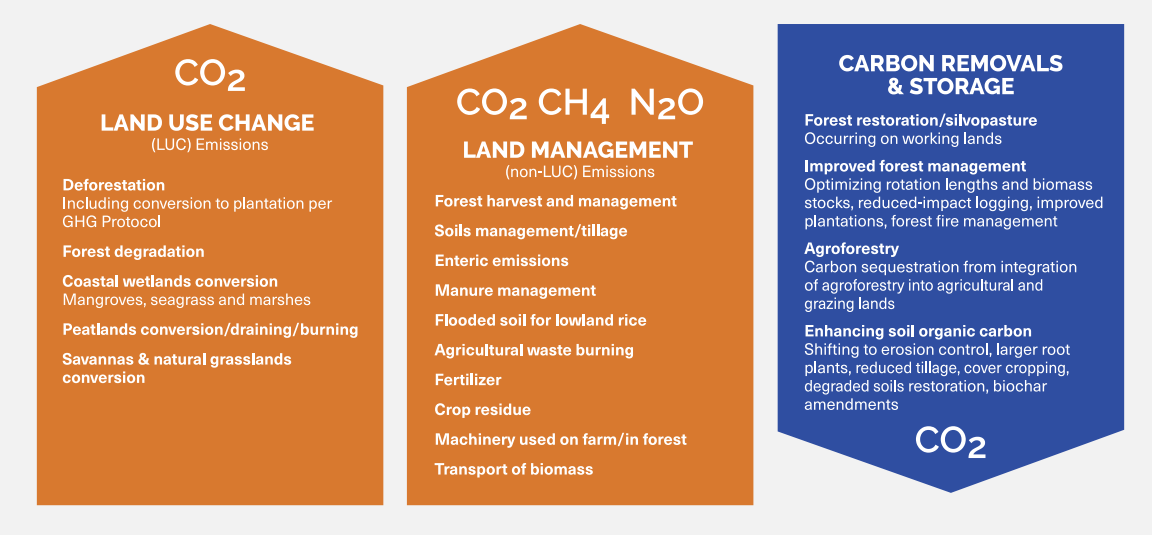

The framework identifies three categories that must be included in a company’s inventory and target.

The first is land use change emissions. This refers to the CO2 released when natural land is converted to agricultural or industrial use, most commonly when forests, wetlands, peatlands, or natural grasslands are cleared. These emissions are typically embedded in the supply chains of food, packaging, and consumer goods companies, even when the company does not own or manage the land directly. Under the standard accounting methodology, these emissions are distributed across a 20-year period following the conversion event.

The second category is land management emissions. These are the ongoing greenhouse gases produced during normal agricultural and forestry operations: methane from livestock digestion and manure, nitrous oxide from fertilizers and crop residues, and CO2 from soil disturbance and forest harvesting. For food and agriculture companies, these emissions typically represent the largest portion of their supply chain footprint.

The third category is carbon removal and sequestration. Forests, soils, and vegetation also absorb carbon from the atmosphere. When a company improves forest management, introduces trees into farmland (agroforestry), restores vegetation on working land, or enhances soil organic carbon, those activities create measurable reductions in atmospheric CO2 that can be credited toward a land emissions target. These removals must be reported separately from emissions reductions. They cannot be used to offset energy or industrial emission obligations under any circumstances.

The Deforestation Commitment: What It Requires and When

One of the most significant requirements in the updated framework is a mandatory public commitment to eliminate deforestation from supply chains. This sits alongside the emissions target itself and carries its own deadlines.

Every company setting land emissions targets must publicly post a commitment stating that it will achieve no deforestation across its primary deforestation-linked commodities, with a stated date for full implementation. That date cannot be later than December 31, 2030.

Companies must also specify a cutoff date. The cutoff date is the point in time after which any deforestation detected in the supply chain is counted as a violation of the commitment. The recommended cutoff is no later than 2020, aligned with globally recognized best practice from the Accountability Framework initiative (AFi, 2023). Where achieving a 2020 cutoff is not possible for specific parts of the supply chain, the cutoff must be at least three years before the company’s first land emissions target submission, and the reasoning must be disclosed publicly. Once set, a cutoff date is fixed and cannot be moved to a later point in time.

For companies that already made a deforestation commitment under earlier versions of this framework, the updated rules recommend maintaining the existing commitment. Companies that choose to update their commitment must set a new target date no later than December 31, 2028, and must publicly disclose what progress they made against the previous commitment, what barriers they encountered, and what actions they plan to address those barriers before revising the commitment.

The assessment of which commodities to include must be thorough. Globally, the commodities most closely linked to deforestation are cattle, cocoa, coffee, oil palm, rubber, soy, and timber (Goldman et al., 2020). Any commodity making up 1% or more of a finished sourced product’s volume must be assessed for inclusion. This means companies with processed or transformed goods in their supply chains need to look through the product composition to identify the underlying commodity exposures.

The framework also recommends, though does not require, that companies make similar commitments to avoid conversion of other natural ecosystems and to eliminate peat burning from supply chains. Meeting a full land emissions target without stopping these practices would be extremely difficult in practice.

Two Ways to Calculate a Land Emissions Target

The framework provides two calculation approaches. The right choice depends on the nature of the company’s supply chain and its position in the value chain.

The sector-wide approach is designed for companies with diverse land-related emissions spread across multiple commodities or geographies, and for companies that sit in the middle or downstream portions of supply chains such as food retailers, processors, and consumer goods companies. It requires an absolute reduction in total land-related emissions over time. The science-based reduction rate is 3.03% per year, which translates to a 30.3% reduction over a ten-year target period. This approach also captures emissions from changes in consumer diets and food waste reduction, making it the most appropriate choice for demand-side companies.

The commodity-specific approach is designed for producers and processors where emissions are concentrated in one or a small number of specific commodities. Rather than measuring total tonnes of CO2, it tracks emissions per unit of production, for example tonnes of CO2 per tonne of beef produced. As production efficiency improves, the emissions intensity falls. This approach is available for eleven commodities: beef, chicken, dairy, leather, maize, palm oil, pork, rice, soy, wheat, and timber and wood fiber. Required annual intensity reduction rates vary by commodity. Companies in the forest products sector with significant timber or wood fiber exposure are required to use this approach for that portion of their emissions.

The two approaches can be combined. Companies with both a diverse supply chain and specific high-concentration commodities are encouraged to aggregate them into a single overall land emissions target.

Required Annual Reduction Rates by Commodity

The table below presents the science-based annual reduction rates for the sector-wide approach and each of the eleven commodity-specific pathways, drawn from the SBTi FLAG Guidance.

| Pathway | Approach Type | Measurement Unit | Reduction Rate (%/yr, 2020–2030) |

|---|---|---|---|

| Sector-Wide Approach | Absolute reduction | tCO₂e | 3.03% |

| Beef | Intensity reduction | tCO₂e / t fresh wt | 2.40% |

| Chicken | Intensity reduction | tCO₂e / t fresh wt | 3.90% |

| Dairy | Intensity reduction | tCO₂e / t fresh wt FPCM | 3.10% |

| Leather | Intensity reduction | tCO₂e / t fresh wt | 2.50% |

| Maize | Intensity reduction | tCO₂e / t fresh wt | 3.50% |

| Palm Oil | Intensity reduction | tCO₂e / t fresh wt | 3.10% |

| Pork | Intensity reduction | tCO₂e / t fresh wt | 3.30% |

| Rice | Intensity reduction | tCO₂e / t fresh wt | 2.90% |

| Soy | Intensity reduction | tCO₂e / t fresh wt | 3.80% |

| Timber & Wood Fiber | Intensity reduction | tCO₂e / m³ | 2.80% |

| Wheat | Intensity reduction | tCO₂e / t fresh wt | 3.60% |

Source: SBTi FLAG Guidance Version 1.2, Table 8, p.60. All figures and labels copied verbatim from source document. The land and agriculture sector is expected to decarbonize more slowly than energy and industry because continued nitrous oxide and methane emissions are more challenging to reduce in agricultural production.

How Land Emissions Targets Fit Into Your Existing Climate Commitments

One of the most practically important aspects of this framework is its relationship to a company’s existing science-based climate targets.

Land emissions targets run in parallel to energy and industrial emissions targets, not in combination with them. A company cannot use reductions in land emissions or carbon sequestration from improved land management to offset its energy-related obligations. Removals from forests or soil count only toward the land emissions target.

This separation applies to reporting as well. Emissions and removals from land must be presented as distinct line items, both in the base year and in annual reporting. A company cannot report a single net land figure without also disclosing the underlying components separately.

For companies that already have validated climate targets, land-related emissions are currently included somewhere in the existing target boundary. When the dedicated land target is established, those emissions are moved into the new framework and the accounting is separated accordingly. The ambition level of the land target, whether classified as a 1.5 degree Celsius or well-below 2 degree Celsius commitment, is determined by the ambition level of the company’s existing energy and industrial target.

Key Deadlines at a Glance

The table below summarizes the most critical compliance deadlines under the updated framework.

| Situation | Requirement | Deadline |

|---|---|---|

| Setting land emissions targets for the first time | Must set a land emissions target upon submission | Already in effect (from April 30, 2023) |

| Company has validated climate targets but no land emissions target | Must set a land emissions target | No later than mandatory five-year review |

| No-deforestation commitment — new submission | Target date for full implementation; cannot exceed the stated ceiling | No later than 31 December 2030 |

| No-deforestation commitment — updating a prior commitment | Set updated target date; publicly disclose prior progress, barriers, and planned actions | No later than 31 December 2028 |

| Publish commitment language on company website | Post method, outcome of commodity assessment, and delivery plan | Within 12 months of validating land emissions target |

Source: SBTi FLAG Guidance Version 1.2, March 2026. All deadline language copied verbatim from source document.

Conclusion

Before a company can set a land emissions target, it needs a land-related GHG inventory. This means calculating the land use change and land management emissions embedded in its supply chains, typically through a combination of supplier data, commodity-level emission factors, and regional sourcing information. This inventory is the prerequisite step, and for most companies it requires engaging either specialist consultants or a platform purpose-built for this type of supply chain emissions measurement.

Once the inventory exists, the target can be calculated using the SBTi’s dedicated tool and submitted for official validation. Validated targets are published on the SBTi website, providing public accountability and a credibility signal to investors, customers, and regulators.

If your organization needs to understand where it stands against these requirements, contact ASUENE today to begin a land emissions readiness assessment.

- Science Based Targets initiative (SBTi). Forest, Land and Agriculture Science-Based Target-Setting Guidance, Version 1.2. March 2026. View source

Why Work with ASUENE Inc.?

ASUENE is a key player in carbon accounting, offering a comprehensive platform that measures, reduces, and reports emissions, including Scope 1-3. ASUENE serves over 10,000 clients worldwide, providing an all-in-one solution that integrates GHG accounting, ESG supply chain management, a Carbon Credit exchange platform, and third-party verification.

ASUENE supports companies in achieving net-zero goals through advanced technology, consulting services, and an extensive network.