- Article Summary

-

Introduction: A Rejection That Signals Deeper Divides

On October 22, 2025, the European Parliament narrowly rejected the compromise text of the EU Omnibus Simplification Package, a proposal intended to streamline sustainability reporting and due diligence rules under the Corporate Sustainability Reporting Directive (CSRD) and the Corporate Sustainability Due Diligence Directive (CSDDD). The result, 318 votes against and 309 in favor, halted what had been expected to be a fast-track agreement with the Council of the European Union. The rejection sent a clear message: many Members of the European Parliament (MEPs) were not ready to endorse a version of the Omnibus that they felt went too far in weakening the EU’s sustainability framework.

European Parliament Vote on the Omnibus Simplification Package (October 22, 2025)

| Vote Category | Number of Votes |

|---|---|

| In Favor | 309 |

| Against | 318 |

| Abstentions | 34 |

This vote was not just a procedural setback; it was a reflection of a broader tension running through Brussels. On one side stood those arguing that European businesses, especially small and medium-sized enterprises, are overburdened by complex ESG regulations. On the other side were those warning that simplification should not come at the cost of climate ambition, human rights due diligence, and transparency. As the Parliament prepares to revisit amendments in November, the rejection has crystallized the EU’s challenge: finding equilibrium between regulatory relief and environmental credibility.

To understand how Europe arrived at this moment, it is necessary to trace the Omnibus Simplification debate from its inception to the present, a process that reveals not only the political calculations behind each step but also what is at stake for companies, investors, and the EU’s global leadership in sustainability regulation.

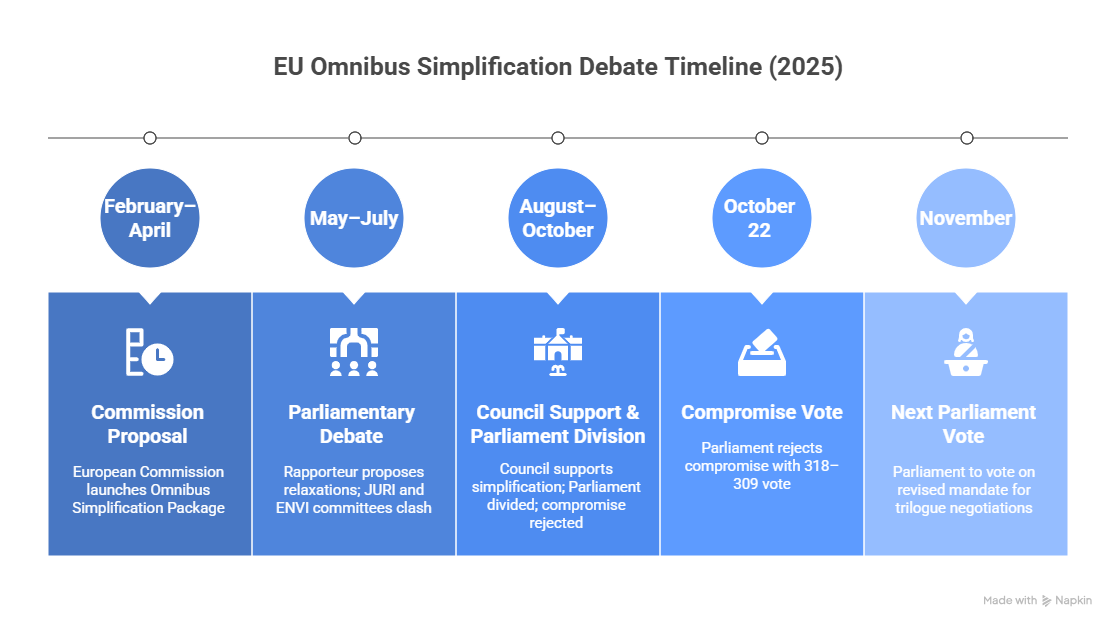

February–April 2025: The Commission Launches the Omnibus Simplification Package

The European Commission unveiled the Omnibus Simplification Package on February 26, 2025, as part of its Competitiveness and Simplification Agenda. The stated objective was straightforward: reduce unnecessary administrative burdens and help firms focus on their core activities. At the heart of the proposal were two main features. First, a “stop-the-clock” mechanism delaying implementation deadlines under the CSRD and CSDDD. Second, revisions to the thresholds defining which companies fall under these directives, raising the bar to firms with at least 3,000 employees or €450 million in annual turnover.

The Commission argued that these measures would allow businesses to adapt more smoothly to sustainability requirements, particularly those still grappling with post-pandemic recovery and higher energy costs. Yet from the beginning, civil society groups and some member states voiced concerns that the simplification effort might undermine the EU’s Green Deal objectives. NGOs warned that relaxing reporting and due diligence thresholds risked excluding thousands of companies whose supply chains significantly impact climate and human rights outcomes.

May–July 2025: Rapporteur Proposals and Parliamentary Debate Intensify

As the proposal entered the parliamentary process, the debate over simplification deepened. The Parliament’s lead rapporteur proposed even broader exemptions, suggesting further increases to reporting thresholds and scaling back transition plan disclosures. Industry groups, especially in manufacturing and retail, welcomed the revisions, arguing that compliance costs had become disproportionate. However, environmental and human rights advocates decried the move as a retreat from the EU’s sustainability commitments.

Inside the European Parliament, divisions grew sharper. The Legal Affairs (JURI) Committee favored pragmatic adjustments, while the Environment (ENVI) Committee pushed back, warning that regulatory dilution would erode the credibility of Europe’s sustainability leadership. During this period, the European Financial Reporting Advisory Group (EFRAG) also began developing drafts of simplified European Sustainability Reporting Standards (ESRS) to align with the Omnibus goals. These technical developments highlighted the Commission’s intention to make ESG compliance more accessible but underscored the risk of creating fragmented or inconsistent reporting frameworks.

August–October 2025: Council Support, Political Fractures, and the Road to Rejection

By late summer, the Council of the European Union had largely aligned with the Commission’s pragmatic stance. Member states expressed support for the stop-the-clock approach and welcomed measures aimed at improving competitiveness amid slowing growth and geopolitical uncertainty. The business community viewed the Council’s position as a necessary recalibration, particularly for non-EU companies seeking clarity on when and how EU sustainability rules would apply.

However, within the European Parliament, political fault lines widened. Centrist and conservative MEPs framed simplification as essential to protecting Europe’s industrial base. Progressive and Green groups countered that the proposal risked hollowing out key sustainability safeguards. The debate became emblematic of broader EU fatigue toward the Green Deal and regulatory expansion. When the compromise text reached the plenary in October, opponents argued that it represented a step backward in transparency and accountability. Their stance ultimately prevailed, setting the stage for another round of negotiations in November.

- Related reading: Check out our earlier analysis, Inside JURI’s ESG Compromise: How the EU’s Omnibus I Vote Dilutes Sustainability Law, to see how the pre-vote debate could have affected the Omnibus outcome.

Looking Ahead: Implications and Next Steps

With the Omnibus proposal rejected, the EU now faces renewed uncertainty. The Parliament will vote again on November 13, 2025, to decide whether to proceed with a revised mandate for trilogue negotiations. Regardless of the outcome, companies must continue preparing for CSRD and CSDDD compliance under the existing frameworks until any changes are formally adopted.

The debate underscores a pivotal question for Europe: can the bloc maintain its global sustainability leadership while responding to calls for regulatory efficiency? For companies, the message is clear: transparency and due diligence remain central expectations, even as policymakers recalibrate the speed and scope of implementation. The Omnibus discussion has shown that simplification is not merely a technical adjustment but a test of the EU’s long-term credibility in linking sustainability, competitiveness, and accountability.

Why Work with ASUENE Inc.?

ASUENE is a key player in carbon accounting, offering a comprehensive platform that measures, reduces, and reports emissions. ASUENE serves over 10,000 clients worldwide, providing an all-in-one solution that integrates GHG accounting, ESG supply chain management, a Carbon Credit exchange platform, and third-party verification.

ASUENE supports companies in achieving net-zero goals through advanced technology, consulting services, and an extensive network.