- Article Summary

-

Overview

In the evolving landscape of environmental regulation, New York has emerged as a pivotal player in advancing corporate climate accountability through Senate Bills 3456 and 3697.

These legislative measures, reintroduced in early 2025, mandate comprehensive greenhouse gas (GHG) emissions reporting and climate-related financial risk disclosures for large corporations operating within the state. This initiative arrives amid federal regulatory rollbacks under the Trump administration, which has sought to dismantle climate disclosure rules previously established by the Securities and Exchange Commission (SEC).

As federal support wanes, New York’s legislation exemplifies a broader trend of state-level climate action, positioning itself alongside California in creating stringent reporting frameworks. This report examines the structural and operational implications of these bills, their alignment with regional efforts, and the legal and economic challenges they face.

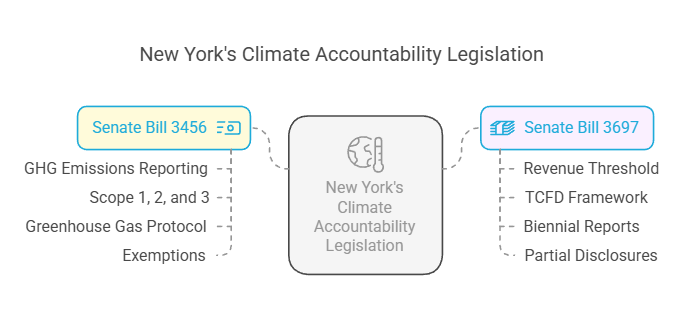

Scope and Requirements of Senate Bill 3456

Senate Bill 3456, the Climate Corporate Data Accountability Act, imposes mandatory GHG emissions reporting for entities with annual revenues exceeding $1 billion that conduct business in New York. The bill mandates annual disclosures of Scope 1 (direct emissions), Scope 2 (indirect emissions from purchased energy), and Scope 3 (value chain emissions) starting in 2027 and 2028, respectively. Reporting entities must adhere to the Greenhouse Gas Protocol’s Corporate Accounting and Reporting Standard, though the legislation permits the New York State Department of Environmental Conservation (DEC) to adopt alternative global standards by 2034 if deemed more effective.

Notably, the bill excludes foreign entities engaged solely in limited activities such as maintaining bank accounts or holding shareholder meetings. This carve-out reflects concerns about extraterritorial enforcement but has drawn criticism from environmental advocates who argue it weakens the law’s comprehensiveness.

Senate Bill 3697: Climate-Related Financial Risk Disclosures

Complementing SB 3456, Senate Bill 3697 targets entities with revenues over $500 million, requiring biennial reports on climate-related financial risks aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework. Covered entities must detail risk mitigation strategies and publish reports on their websites, ensuring transparency for investors and stakeholders. The bill allows flexibility for companies lacking complete data, permitting partial disclosures with explanations of gaps and remediation plans.

Enforcement and Funding Mechanisms

Both bills introduce financial penalties for noncompliance, though specific amounts remain undefined. SB 3456 authorizes the DEC to impose annual fees on reporting entities to fund administrative costs, creating a dedicated Climate Accountability and Emissions Disclosure Fund. This self-sustaining model mirrors California’s approach but raises concerns about disproportionate burdens on out-of-state corporations.

SEC’s Retreat from Climate Disclosure Rules

The SEC’s climate disclosure rule, finalized in 2024 under Chair Gary Gensler, required public companies to report climate risks and emissions data in regulatory filings. However, Acting Chair Mark Uyeda halted the rule’s defense in February 2025, calling it “deeply flawed” and beyond the SEC’s statutory authority. This reversal aligns with the Trump administration’s broader deregulatory agenda, which has targeted EPA emissions standards and clean energy incentives.

Implications for Corporate Compliance

The SEC’s retreat creates a regulatory vacuum, compelling states like New York and California to establish their own frameworks. While federal inaction reduces immediate compliance burdens for multinational firms, it exacerbates fragmentation as companies navigate conflicting state requirements. For instance, California’s SB 253 mandates Scope 3 reporting for firms with over $1 billion in revenue, overlapping with New York’s SB 3456 but differing in enforcement timelines.

The Climate Superfund Act Litigation

New York’s Climate Superfund Act, enacted in December 2024, faces a multi-state lawsuit alleging constitutional violations. Plaintiffs argue the Act’s retroactive fines on fossil fuel producers violate the Commerce Clause by penalizing out-of-state entities for lawful activities. The lawsuit also cites Due Process and Takings Clause violations, contending the law’s penalties are excessive and lack sufficient nexus to New York’s climate damages.

Preemption and Interstate Tensions

The litigation underscores tensions between state climate policies and federalism principles. Critics argue that New York’s laws infringe on the Clean Air Act’s federal preemption doctrine, which reserves emissions regulation to the EPA. However, proponents counter that disclosure mandates fall outside traditional environmental regulation, occupying a permissible space under state consumer protection laws.

California-New York Synergy

New York’s legislation closely mirrors California’s SB 253 and SB 261, creating a de facto regional standard for climate disclosures. Both states prioritize Scope 3 reporting, recognizing that value chain emissions often constitute the majority of a company’s carbon footprint. However, California’s earlier implementation timeline (2026 vs. New York’s 2027) risks creating compliance bottlenecks for firms operating in both jurisdictions.

Northeastern Clean Energy Collaboration

New York’s participation in the Regional Greenhouse Gas Initiative (RGGI) provides a model for multi-state climate governance. The state’s offshore wind investments, including the 4.3 GW Sunrise Wind project, align with RGGI’s emissions reduction targets but face delays due to federal permitting hurdles.

Compliance Costs and Operational Challenges

For affected companies, SB 3456 and 3697 necessitate significant investments in data collection systems, particularly for Scope 3 emissions, which involve complex supply chain tracking. A 2025 analysis by the U.S. Chamber of Commerce estimates initial compliance costs at $2–$5 million annually for large corporations, with ongoing expenses tied to third-party audits.

Opportunities for ESG Leadership

Proactive firms can leverage disclosures to enhance investor confidence and access green financing. Companies like Microsoft and Unilever have already aligned their reporting with TCFD, positioning themselves as sustainability leaders. However, inconsistent state requirements risk diluting the comparability of ESG metrics, complicating investment decisions.

Why Not Work with ASUENE USA Inc.?

When it comes to navigating New York’s complex climate disclosure requirements, it is crucial to have the right tools and expertise on your side. That’s where ASUENE USA Inc. comes in.

Carbon Accounting: Our advanced software solutions automate emissions tracking across Scopes 1, 2, and 3, integrating with existing ERP systems to reduce manual data entry errors. Proprietary algorithms align with GHG Protocol standards, ensuring compliance with ESG reporting mandates.

Third-Party Verification: ASUENE’s network of accredited auditors provides ISO 14064-compliant verification services, a critical step for companies seeking to validate their disclosures under New York’s legislation.

Consulting Services: Our team offers tailored guidance on TCFD-aligned risk reporting, helping firms identify material climate risks and craft mitigation strategies that satisfy disclosure requirements.

By partnering with ASUENE USA, businesses can transform regulatory obligations into strategic advantages, enhancing sustainability performance while minimizing compliance costs.

So, why not partner with us to streamline your reporting and environmental efforts? Let ASUENE USA Inc. help you stay ahead of the curve while making a positive impact on both your business and the planet.