- Article Summary

-

Overview

Financial institutions increasingly face expectations to measure and disclose the climate impact of their portfolios.

For banks, investors, and insurers, financed emissions linked to lending, investments, and underwriting activities are often far larger than operational emissions.

To address this challenge, the Partnership for Carbon Accounting Financials (PCAF) provides standardized methodologies for measuring emissions associated with financial activities. The framework helps improve transparency, comparability, and accountability across the financial sector.

Key Takeaways

- The Partnership for Carbon Accounting Financials (PCAF) is an industry led initiative that provides standardized methodologies for financial institutions to measure and disclose emissions associated with financial activities.

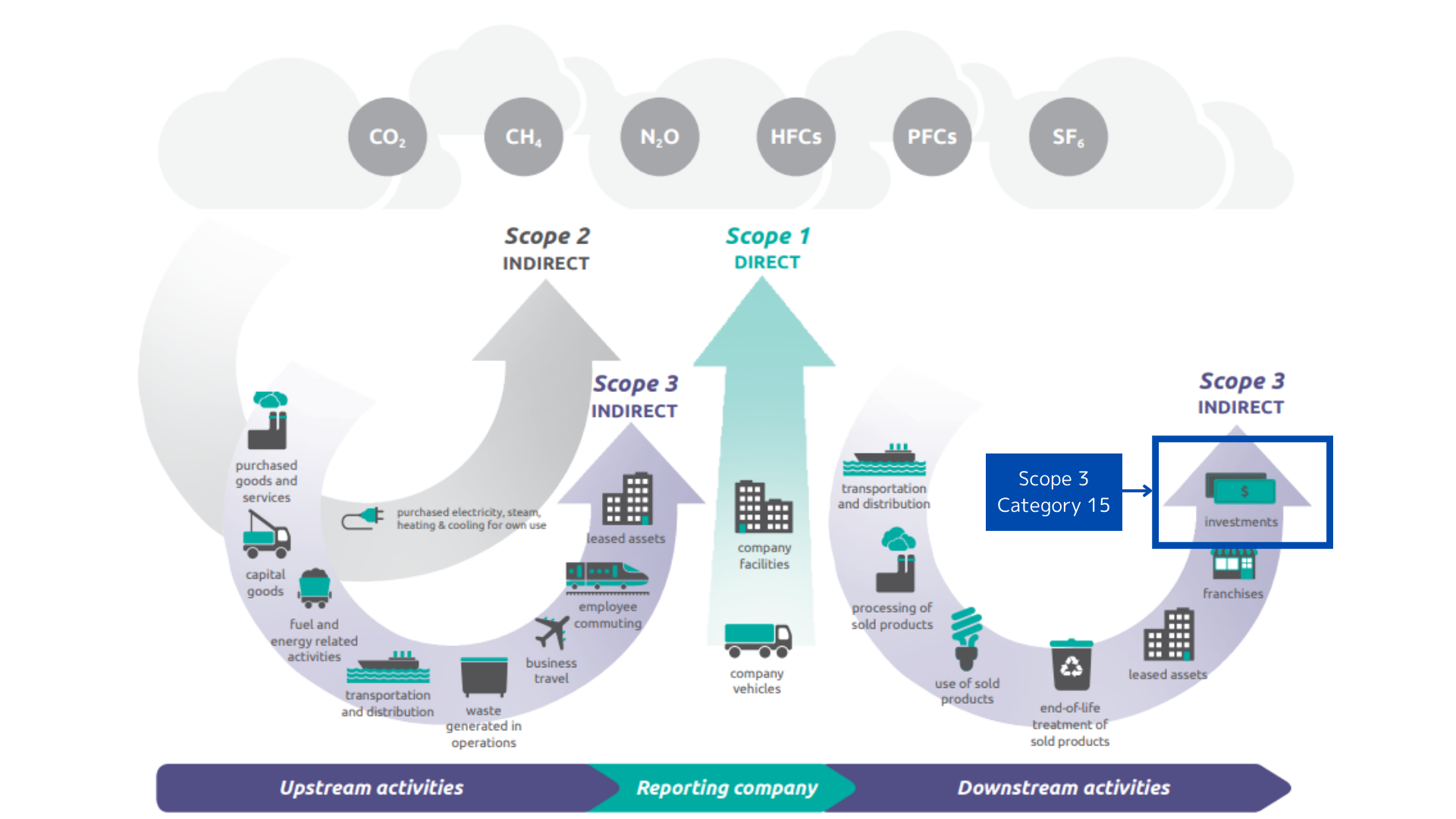

- The framework focuses on Scope 3 Category 15 emissions, which typically represent the largest share of emissions linked to financial institutions.

- The PCAF standard consists of three parts covering financed emissions, facilitated emissions, and insurance associated emissions.

- The 2025 update expanded the financed emissions methodology to ten asset classes and introduced additional reporting guidance.

- The standard supports climate disclosure frameworks and helps financial institutions improve transparency, comparability, and portfolio level emissions analysis.

What Is PCAF?

PCAF at a Glance

PCAF (Partnership for Carbon Accounting Financials) is an industry‑led initiative that provides standardized methodologies for financial institutions to measure and disclose emissions associated with financial activities.

PCAF mission

- Standardize greenhouse gas accounting across the financial sector

- Enable institutions to measure Scope 3 Category 15 (investments) emissions

- Improve transparency and comparability of financed emissions data

- Support climate disclosure and portfolio level emissions analysis

Why Financed Emissions Matter

For most financial institutions, financed emissions represent the largest share of their climate impact.

Measuring these emissions helps institutions:

- understand the carbon intensity of their portfolios

- identify exposure to high‑emitting sectors

- assess climate related financial risks

Financial emissions accounting therefore plays an important role in climate disclosure, risk management, and portfolio strategy.

The PCAF framework enables financial institutions to measure emissions linked to loans, investments, capital market activities, and insurance underwriting.

By applying consistent accounting rules, institutions can calculate their share of portfolio emissions and disclose those results in sustainability and climate reports.

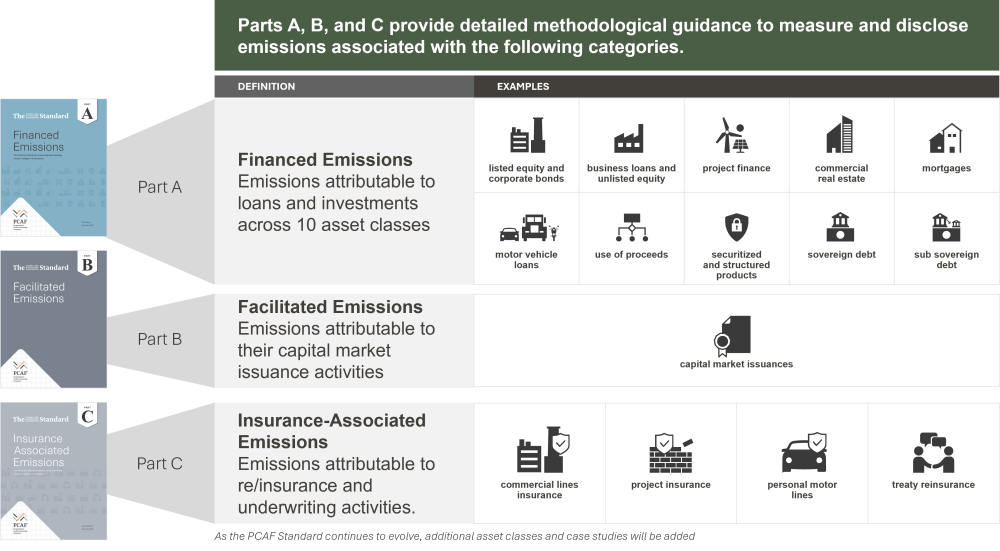

Structure of the PCAF Standard

The PCAF Global GHG Accounting and Reporting Standard for the Financial Industry is organized into three methodological parts. Each part addresses emissions associated with a different type of financial activity.

| PCAF Standard | Definition | Primary Users |

|---|---|---|

| Part A: Financed Emissions | Standard for measuring and reporting emissions associated with loans and investments | Banks, asset managers, development banks, and other financial institutions |

| Part B: Facilitated Emissions | Standard for measuring emissions linked to capital market facilitation activities | Investment banks and financial institutions arranging debt or equity issuance |

| Part C: Insurance Associated Emissions | Standard for measuring emissions associated with insurance underwriting portfolios | Insurance companies and reinsurance companies |

Part A: Financed Emissions

Part A focuses on emissions associated with loans and investments held on financial institutions’ balance sheets. These emissions are typically reported under Scope 3 Category 15 and represent the most significant share of climate impact for many financial institutions.

Following the latest expansion of the standard, Part A now covers ten asset classes.

The expansion reflects the growing diversity of financial instruments used across global markets and PCAF’s mission to standardize greenhouse gas accounting across the financial sector.

Part B: Facilitated Emissions

Part B addresses emissions linked to capital market facilitation activities. These include services provided by financial institutions to support the issuance of bonds, equities, and syndicated loans. In these cases, institutions typically arrange transactions rather than provide long term financing directly.

By measuring facilitated emissions, banks can assess the climate impact associated with capital market activities that enable companies and governments to raise funding. This approach improves transparency around the role financial institutions play in directing capital toward different sectors of the economy.

Part C: Insurance Associated Emissions

Part C focuses on emissions associated with insurance underwriting portfolios. Insurance coverage often enables economic activities that carry environmental impacts, making it important for insurers to measure emissions linked to insured assets and operations.

The methodology provides insurers and reinsurers with a structured approach to calculate emissions associated with commercial insurance portfolios, project insurance, personal motor insurance, and treaty reinsurance portfolios.

Recent Updates to the PCAF Standard

PCAF released a major update to its Global GHG Accounting and Reporting Standard in December 2025. The revision expands the coverage of financed emissions methodologies and introduces additional reporting guidance to improve comparability and transparency across financial institutions.

Key Updates in the 2025 PCAF Revision

| Update Area | Description |

|---|---|

| Expanded asset classes | The financed emissions methodology now covers ten asset classes, including securitizations and structured products, use of proceeds structures, and sub sovereign debt. |

| New methodologies | Additional calculation guidance was introduced for financial instruments that were not covered in earlier versions of the standard. |

| Enhanced reporting guidance | New recommendations such as fluctuation analysis and inflation adjustments help institutions explain changes in portfolio emissions over time. |

| Alignment with disclosure frameworks | The updated guidance helps financial institutions align emissions reporting with climate disclosure frameworks such as ISSB standards and CDP reporting. |

These updates reflect the growing role of emissions accounting in financial sector climate disclosure and portfolio risk analysis.

How PCAF Relates to Other Climate Frameworks

PCAF does not operate as a standalone disclosure framework. Instead, it provides the technical methodology that supports several widely used climate reporting standards in the financial sector.

To understand its role, it helps to see how PCAF connects with three major frameworks used by financial institutions.

GHG Protocol

The PCAF methodologies are built on the GHG Protocol, particularly the Corporate Value Chain (Scope 3) Accounting and Reporting Standard. While the GHG Protocol defines how organizations report Scope 3 emissions, it provides limited guidance for financial institutions on calculating emissions linked to investments and financial services.

PCAF fills this gap by offering detailed calculation methodologies for Scope 3 Category 15 emissions, enabling banks and investors to quantify the emissions associated with their portfolios.

ISSB and TCFD Climate Disclosure Frameworks

PCAF also supports broader climate disclosure standards such as the International Sustainability Standards Board (ISSB) climate disclosure framework, which builds on the former Task Force on Climate-related Financial Disclosures (TCFD) recommendations.

By applying PCAF methodologies, financial institutions can generate consistent financed emissions data that can be used in climate disclosures under these frameworks.

CDP Climate Disclosure

The PCAF standard also plays an operational role in CDP climate reporting. The Global GHG Accounting and Reporting Standard supports financial institutions responding to CDP disclosure requests by providing clear methodologies and calculation guidance.

CDP cites PCAF as a key reference standard for measuring and reporting financed emissions, helping ensure consistency and comparability across institutions.

Why PCAF Is Becoming the Global Standard

Several factors have contributed to the growing adoption of PCAF across the financial sector:

- Financed emissions dominate financial sector footprints

Financed emissions typically represent the largest portion of a financial institution’s climate impact. - Increasing climate disclosure expectations

Regulators, investors, and stakeholders increasingly expect financial institutions to disclose the climate impact of their portfolios. - Climate risk management

Measuring financed emissions helps institutions identify carbon intensive sectors and evaluate transition risks. - Expansion of the standard

The continued expansion of the PCAF framework has strengthened its relevance across financial products and institutions.

Conclusion

PCAF has emerged as a key methodology for measuring emissions associated with financial activities. By providing standardized approaches to calculate financed, facilitated, and insurance-associated emissions, the framework helps financial institutions improve transparency and comparability in climate reporting.

As climate disclosure expectations continue to evolve, PCAF is likely to remain an important reference for institutions seeking to understand and manage the emissions linked to their portfolios.

Sources

- Partnership for Carbon Accounting Financials (PCAF), The Global GHG Accounting and Reporting Standard for the Financial Industry

- Partnership for Carbon Accounting Financials (PCAF), The Global GHG Accounting and Reporting Standard – Official Standard Page

Why Work with ASUENE Inc.?

ASUENE is a key player in carbon accounting, offering a comprehensive platform that measures, reduces, and reports emissions, including Scope 1-3 and PCAF based disclosures. ASUENE serves over 10,000 clients worldwide, providing an all-in-one solution that integrates GHG accounting, ESG supply chain management, a Carbon Credit exchange platform, and third-party verification.

ASUENE supports companies in achieving net-zero goals through advanced technology, consulting services, and an extensive network.