- Article Summary

-

Introduction: A New Chapter for SME Sustainability Reporting in Europe

On July 30, 2025, the European Commission took an important step toward broadening access to ESG disclosure by adopting a Recommendation on the use of the Voluntary Sustainability Reporting Standard for non-listed SMEs, commonly referred to as VSME. The standard was developed by the European Financial Reporting Advisory Group (EFRAG), an independent body tasked with supporting the implementation of the Corporate Sustainability Reporting Directive (CSRD). The Recommendation aims to help small and medium-sized enterprises navigate rising expectations for transparency from large buyers, financial institutions, and regulators.

The VSME is positioned as a flexible and accessible tool to guide SMEs through the fundamentals of sustainability reporting. While the Recommendation is non-binding, its publication signals strong institutional support for a more inclusive approach to ESG reporting. It also points toward a future in which supply chain transparency becomes a shared responsibility, not just a top-down requirement.

The Role of EFRAG and the Scope of the VSME Standard

EFRAG developed the VSME standard under a CSRD mandate to provide a proportionate and relevant reporting framework for smaller businesses. The standard is targeted specifically at non-listed SMEs that fall outside the mandatory scope of the CSRD. These businesses are not legally required to report under the CSRD but may face increasing demand for ESG information from clients, investors, and banks. The VSME standard offers them a structured way to respond.

The VSME framework takes a modular and simplified approach. It addresses essential sustainability topics, including climate, water, social impact, and governance. Instead of requiring exhaustive data collection, it emphasizes narrative responses and a limited set of indicators. This approach lowers the reporting burden for SMEs that may lack the capacity or resources of larger firms.

While voluntary, the VSME standard has been designed to align with the ESRS under the CSRD. This conceptual alignment ensures that the information disclosed by SMEs can be more easily integrated into the reporting frameworks used by larger companies. The result is better consistency, comparability, and utility of ESG data across supply chains and financial systems.

| Feature | VSME | ESRS |

|---|---|---|

| Legal Status | Non-binding Recommendation | Legally binding via CSRD |

| Target Companies | Non-listed SMEs | Large companies and listed SMEs |

| Reporting Burden | Low to moderate | High |

| Use Case | Supply chain response, B2B ESG | Regulatory compliance |

The Commission’s Recommendation vs. a Future Delegated Act

It is essential to distinguish between the Commission’s current Recommendation and the formal adoption of a Delegated Act, which would give the VSME standard legal standing under Article 29c(2) of the CSRD. As of July 2025, the Commission has not yet adopted such a Delegated Act. Instead, it has issued a policy-level endorsement encouraging voluntary uptake.

This nuance was acknowledged directly by the Commission, which noted that “the content of the future voluntary reporting standard might differ from the current VSME Recommendation.” This reflects the ongoing nature of field testing and stakeholder consultation. Feedback collected during this interim phase may shape the final text of the Delegated Act, expected in 2026.

The distinction is not just procedural. A Delegated Act would establish the VSME as an official reporting option under EU law, with implications for procurement, investment, and third-party assurance. The Recommendation, by contrast, is an interim measure to facilitate early engagement and voluntary experimentation.

| Timeline | Key Milestone |

| 2023–2025 | EFRAG develops draft VSME standard |

| July 30, 2025 | EU Commission adopts Recommendation |

| 2025–2026 | Field testing and public consultation continue |

| Expected 2026+ | Commission may adopt Delegated Act based on final VSME |

What VSME Means for Supply Chains, Scope 3 Emissions, and ESG Strategy

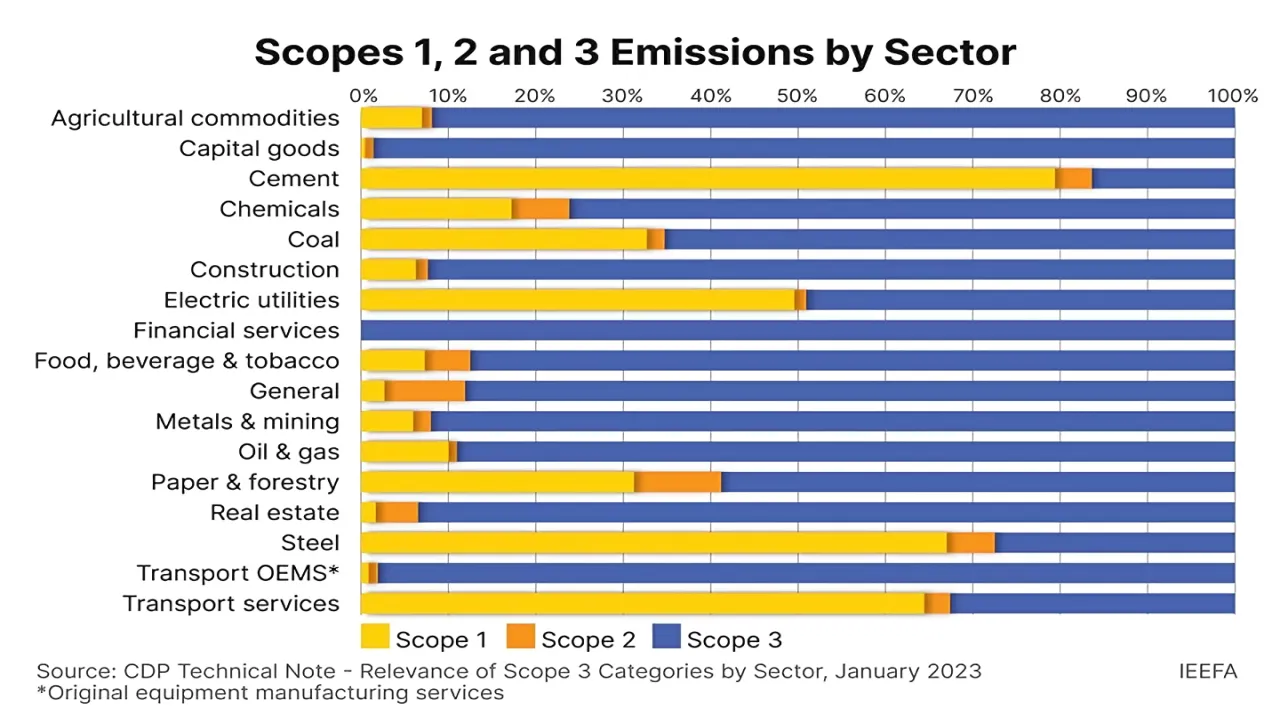

Large companies preparing CSRD disclosures face the challenge of collecting data from suppliers, many of whom are SMEs. These upstream actors represent a significant portion of Scope 3 emissions, particularly in sectors like manufacturing, apparel, and technology. The availability of a standardized, voluntary template like the VSME makes it easier for small suppliers to respond to ESG requests without incurring high compliance costs.

For SMEs, the VSME standard offers a structured way to build internal capacity and respond to due diligence questionnaires, especially from multinational clients. For buyers and investors, it improves comparability and reliability across supplier disclosures.

Studies show that in industries such as manufacturing and consumer goods, more than 75% of total emissions reside in the value chain (scope 3).

VSME can serve as a bridge between regulatory requirements and practical constraints. It provides a foundation for common language, which in turn supports better risk assessment, greener procurement, and more resilient supply chains.

Conclusion: From Voluntary to Valuable

The VSME framework arrives at a time when sustainability reporting is evolving from a niche concern into a baseline expectation. While the standard remains voluntary for now and is still subject to refinement, it adds important value for a wide range of stakeholders.

For SMEs, it provides clarity and consistency in a landscape crowded with disparate ESG requests. For large enterprises, it offers a practical mechanism to engage suppliers and improve Scope 3 visibility. For policymakers and standard-setters, it reflects an effort to ensure that ESG transparency does not become a barrier to SME participation in the green transition.

The VSME Recommendation does not impose new obligations. It introduces a flexible tool with the potential to support more meaningful dialogue and better sustainability outcomes across the business ecosystem. Its future will depend not only on regulatory action but also on how companies and stakeholders choose to engage with it today.

Continue reading about VSME:

VSME Framework: Practical Guide with Difference from ESRS

VSME: Voluntary Sustainable Reporting Standard for non-listed SMEs

Why Work with ASUENE Inc.?

Asuene is a key player in carbon accounting, offering a comprehensive platform that measures, reduces, and reports emissions. Asuene serves over 10,000 clients worldwide, providing an all-in-one solution that integrates GHG accounting, ESG supply chain management, a Carbon Credit exchange platform, and third-party verification.

ASUENE supports companies in achieving net-zero goals through advanced technology, consulting services, and an extensive network.